SEBI Debt Fund Rules 2026: Debt Funds Masterclass - Duration, Credit Risk, Yields Guide

SEBI 2026 updates: Debt Macaulay duration bands, Credit Risk 65% AA-, Sectoral Debt. Risks vs yields table + Gilt vs Corporate Bond picks for balanced portfolios.

Reading time: about 2 minutes

Building on our equity deep dive, let’s tackle debt funds—the steady stabilizers in volatile markets. Debt is like reliable, low-drama returns (6-8% CAGR) to balance equity sprints. SEBI’s February 26, 2026, circular ties debt to precise Macaulay duration bands, making choices crystal clear.

This post explains the updates, risks vs. yields, and smart picks like Gilt over Corporate Bonds.

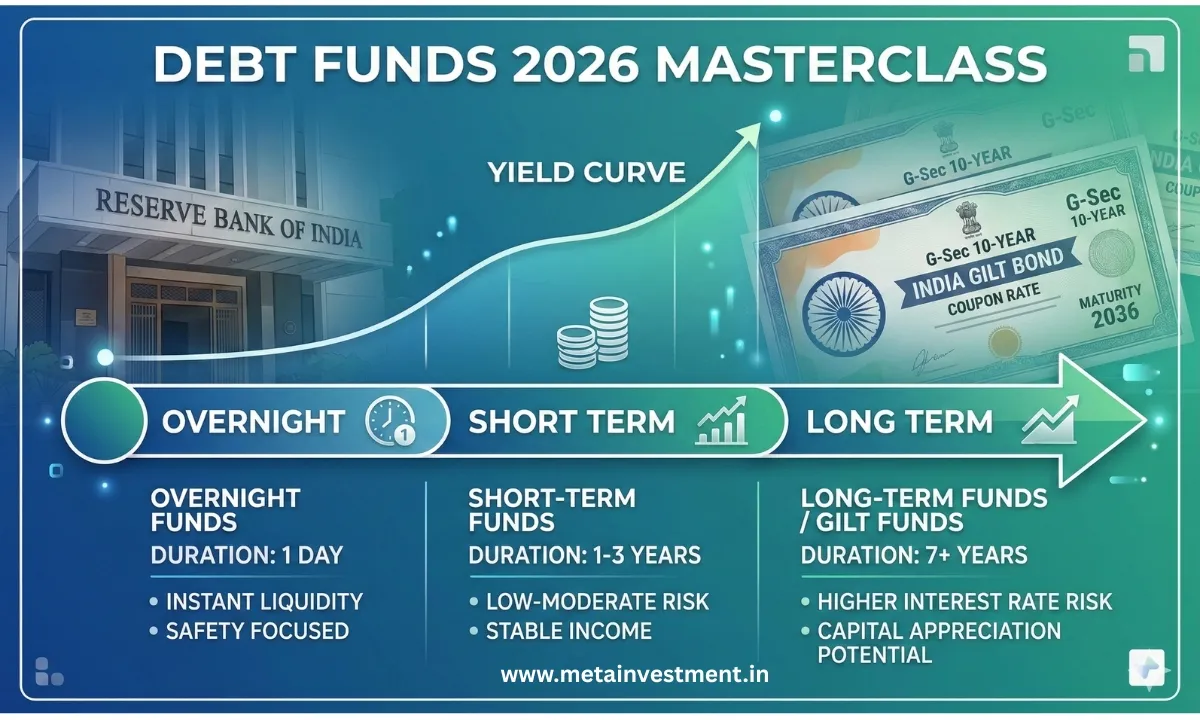

New Debt Fund Categories Explained

SEBI now mandates Macaulay duration (weighted average time to cash flows) for transparency—no more vague “short-term” labels. Here’s the breakdown:

- Overnight Fund: 1-day maturity securities. Ultra-safe parking.

- Liquid Fund: Up to 91 days maturity. Cash equivalent.

- Short Term Fund: 1-3 years Macaulay duration. Balanced yield-risk.

- Credit Risk Fund: ≥65% in AA and below rated corporate bonds (ex-AA+). Higher yield chase.

- Sectoral Debt Fund: ≥80% in sectors like Financial Services, Energy (AA+ only). Niche plays.

- Gilt Fund: ≥80% government securities. Sovereign safety.

Key Idea: Duration bands predict interest rate sensitivity—shorter = less NAV drop when rates rise. Reasoning: Post-2022 rate hikes crushed loose labels; now investors know exact risk.

Risks, Yields, and When to Choose What

Debt isn’t “risk-free”—credit events (e.g., DHFL) and rate cycles matter.

| Fund Type | Typical Yield (2026 est.) | Key Risk | Best For |

|---|---|---|---|

| Short Term | 7-7.5% | Moderate rate risk | 1-3 yr goals; parking lump sums |

| Credit Risk | 8-9% | Default in AA-/A bonds | Yield hunters (5%+ credit spread) |

| Sectoral (Fin Svcs) | 7.5-8.5% | Sector downturns | Bank/PSU bulls; max 10% portfolio |

| Gilt Fund | 6.5-7.5% | High rate sensitivity | Rate fall bets; tax-free options |

Insight: Choose Gilt over Corporate Bond when expecting rate cuts (RBI signals)—Gilts rally 5-10% on 1% rate drop, zero credit risk. Corporate shines in stable rates (AA+ safety + 1-2% spread).

Yields Reasoning: 2026 10-yr G-Sec ~7%; credits add spread but volatility (e.g., Credit Risk drew 25% in 2020 defaults).

Suitability for Balanced Portfolios

- Conservative (50+ age): Overnight/Liquid (0-12 month needs).

- Moderate: Short Term + Banking/PSU (laddering).

- Yield Seekers: Credit Risk (diversify across 20+ funds). Avoid Sectoral unless convicted (e.g., infra boom).

Pro Tip: In rising rates (like 2022-24), shorten duration to 1-3 years. Post-peak, extend to Medium (3-4 years).

Action Steps for Debt Review

- Map holdings to duration bands via factsheets.

- Cap Credit Risk at 15% portfolio; stress-test defaults.

- Ladder: 30% Short + 30% Medium + 40% Long.

- Watch RBI Feb 2026 policy for Gilt triggers.

Gold note: Exchange spot pricing (April 1) stabilizes commodity debt tangentially.

Part 1: SEBI Mutual Fund Changes 2026: The Big Picture Explained

Part 2: Equity Funds Deep Dive

Next: Hybrid Strategies Updated. Subscribe for the series, share with your investor group, or WhatsApp for a debt audit!

Disclaimer: Not investment advice. Consult a SEBI-registered advisor.

Frequently Asked Questions

What are SEBI's new debt fund duration bands?

Funds now follow strict Macaulay duration rules—Overnight (1-day), Liquid (up to 91 days), Short Term (1-3 years), Medium Term (3-4 years), Long Term (>7 years).

What defines Credit Risk Funds under 2026 rules?

Minimum 65% investment in corporate bonds rated AA and below (excluding AA+), chasing higher yields through lower-rated paper.

Which sectors can Sectoral Debt Funds target?

Financial Services, Energy, Infrastructure, Housing, Real Estate—minimum 80% allocation in AA+ rated bonds from those sectors.

When should I choose Gilt Funds over Corporate Bond Funds?

Pick Gilts (80%+ G-Secs) for expected rate cuts or zero credit risk; Corporate Bonds suit stable rates with 1-2% extra yield.

What are typical yields for Short Term debt funds?

Around 7-7.5% in 2026 estimates, balancing moderate rate risk—ideal for 1-3 year goals or lump sum parking.

How does Macaulay duration affect my debt fund?

Measures interest rate sensitivity—shorter durations (1-3 years) mean smaller NAV drops when rates rise.

What risks come with Credit Risk Funds?

Higher default potential in AA-/A bonds, but diversification across funds mitigates; expect 8-9% yields.

Can debt funds invest in InvITs now?

Yes, residual portion allowed (except Overnight/Liquid/Ultra Short), subject to MF regulations ceilings.

How to ladder debt funds post-SEBI changes?

Spread across Short (30%), Medium (30%), Long (40%) to manage rate risk and steady income.

Will RBI rate cuts boost all debt funds equally?

No—longer duration funds (Gilt, Long Term) rally more (5-10% on 1% cut); shorten in rising rate cycles.

(Updated: )

0

")